Diane’s farewell message

After 52 years at WAMU, Diane Rehm says goodbye.

Guest Host: Susan Page

This October 25, 2016 photo shows a woman looking at the Healthcare.gov internet site in Washington, D.C. Americans will see Obamacare health insurance costs jump an average of 25 percent next year, adding fuel to the U.S. political firestorm over the system that Republicans have repeatedly tried to overturn.

Twenty million Americans have gained health insurance under the Affordable Care Act. But as it prepares for its fourth open enrollment season next week, the ACA faces perhaps its biggest test yet. Premiums for plans purchased through the exchanges are expected to rise an average of 25 percent next year. And some insurers are pulling out of the marketplace. The news is fueling debate on the campaign trail over the signature piece of President Barack Obama’s legacy and how it improve it—a task that will soon be left to a new president and Congress. A look at where the Affordable Care Act is going and how a new president might change it.

MS. SUSAN PAGEThanks for joining us. I'm Susan Page of USA Today sitting in for Diane Rehm. She's in New York to receive a lifetime achievement award from the International Women's Media Foundation. Our congratulations to Diane for that. Next week, consumers who purchase insurance through the Affordable Care Act will log onto Healthcare.gov to find premiums that are, on average, 25 percent higher than they were last year. We'll talk about what that means for consumers and for the future of Obamacare under a new administration.

MS. SUSAN PAGEWith me in the studio, Julie Rovner, senior correspondent at Kaiser Health News, Ron Pollack, executive director of Families USA and Avik Roy, president of the Foundation for Research on Equal Opportunity. He's a former policy advisor to Mitt Romney, Marco Rubio and Rick Perry. Welcome to you all.

MR. AVIK ROYDelighted to be with you again.

MS. JULIE ROVNERThank you.

MR. RON POLLACKThank you.

PAGEWe're going to invite our listeners to join our conversation in just a bit. Our toll-free number 1-800-433-8850. You can always send us an email to drshow@wamu.org or find us on Facebook or Twitter. So Julie, on Monday, the government announced these higher average premium rates for 2017, 25 percent in a year sounds like a lot. Is this a surprise?

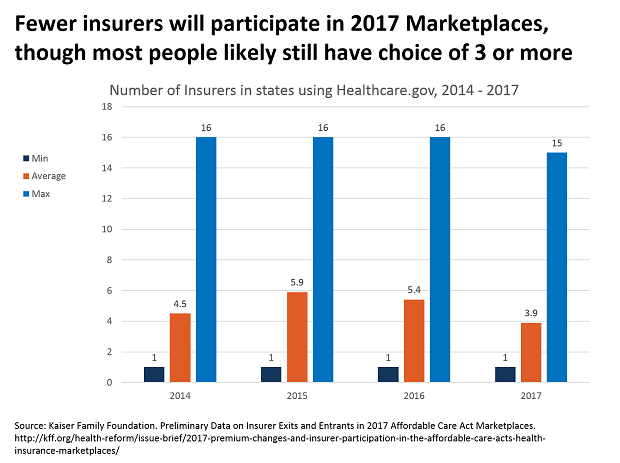

ROVNERIt's not a surprise. We've known it was coming. Really, there's kind of a perfect storm that's happened this year. There's a couple of temporary programs that were supposed to help insurers, you know, because a lot of insurers didn't have any idea how this market was going to work. Two of those three temporary programs are expiring. In some states, insurers just guessed wrong that they set their premiums too low and there has been not as robust enrollment for a lot of -- for reason we can talk about later -- as people had hoped.

ROVNERAnd those three things really, together, are contributing to these higher premiums. I should point out, though, that that is an average and it's like, you know, saying how can you drown in a lake where, you know, the average depth is two feet. In some places, the premiums are going up a whole lot and in some places they're even going down.

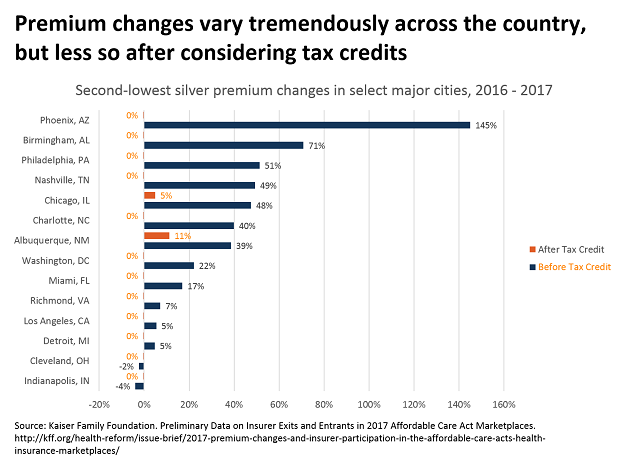

PAGEOn our website, we've posted a graphic from Kaiser Foundation that shows premium increases by state and the range is incredible. Some states' premiums are actually going down, but as you say, in a place like Arizona, it just seems to be skyrocketing. So what is this going to mean, Avik Roy, for consumers, for people who are using these exchanges?

ROYYeah, so I think one thing that we can talk about is that it's not just this year when we've seen premium increases. So for the four years that we've had these Affordable Care Act exchanges, premiums have gone up, on average, every year at a level or a rate that exceeds normal healthcare inflation. So the cumulative impact from 2013 to 2017 is over 100 percent on average in terms of the premium increases for people who are purchasing coverage on their own. And the result of that has been that fewer people are enrolling in the exchanges than we expected or that the Congressional Budget Office expected in 2010.

ROYSo in 2010, the CBO projected that 21 million people would be enrolled in exchanges in 2016. The actual number was more like 12 million. And the question we have going forward, or the concern we have going forward, is as these premiums continue to rise, does the enrollment in the exchanges flatten out? Do we no longer see the growth enrollment in the next several years?

PAGEWell, what do you think, Ron Pollack? First of all, the first word of this law is "affordable," the Affordable Care Act. Is it proving not to be affordable for people who are buying their insurance through these exchanges?

POLLACKWell, it has to be understood that in terms of how a consumer is going to feel affected by it, they're not going to look so much at what the premium is. They're going to look at what their out-of-pocket cost is. And that's why you have to take into consideration not just what's happening with the premium, but also what's happening with the subsidies they are receiving in order for them to afford coverage. Now, I think for your listeners, the first thing they really need to understand is the vast majority of people who have health insurance are not going to be affected by it.

POLLACKYou've got about half the people who have health insurance have employer sponsored health insurance. They are not affected by this. Those who are on Medicare and Medicaid -- that's a large number. Medicaid alone, it's 72.5 million people. They're not going to be affected by it. So the focus is on those people who are buying individual coverage in the marketplace and there are approximately 11 million people. The vast majority of these people receive very significant subsidies that make coverage affordable.

POLLACK85 percent of the people who are in these marketplaces are getting subsidies. So as the premiums go up, so do the subsidies and so in terms of the out-of-pocket costs that folks bear, they're not going to see much of a difference.

PAGEWell, so Ron, that's great for the people who are getting subsidies, but does that mean taxpayers have to pay more because the premiums are going up and so the subsidies are rising?

POLLACKWell, the group that's going to be most directly affected are those who are in the individual marketplace who don't get subsides. And there are approximately 1.5 million people who are in that group. These are folks who have incomes above 400 percent of the federal poverty level. So for a family of four, we're talking about a family that has income in excess of $97,000. So there's no question that as the subsidies go up, there will be some additional revenues that will have to be spent in terms of subsidizing, but the bottom line with respect to the healthcare consumer -- because you asked is this going to be affordable for them -- it will be affordable for them.

PAGEJulie.

ROVNERWell, two things. First of all, interestingly, because, as we talked about, there's been less enrollment than was expected, even with these increased premiums and the subsidies will now go up correspondingly, it will still only be about the same as CBO projected. CBO didn't project beyond 2016, but people who have done the math say it won't -- it's not going to bust the budget on this. But I think the other thing that's really important to keep in mind is that, yes, the subsidies go up for the premiums so people -- most people who get subsidies will be held harmless on their premiums.

ROVNERBut as Ron pointed out, it's not just the premiums. It's also the out-of-pockets costs and even people -- many people who are getting premium subsidies are not getting help with their out-of-pocket costs so they may be able to afford the premiums, but then they're going to end up with a deductible of $7,000 and that's, I think, probably a bigger issue going forward than the premiums that everybody's looking at right now.

ROYYes. I would add two points to what Julie and Ron were saying. First of all, it's important to note that the subsidies that -- the cushion that the subsidies provide to those who are at the lower end of the income scale is relatively temporary because there's an obscure provision of the ACA in which the growth of subsidies over the long term is index to a formula that resembles inflation, which means that if premiums continue to go up at a high rate, much higher than inflation, the subsidies will not keep pace with premium growth and that will be a significant problem for the sustainability of the exchanges over the long term.

ROYAnother point that I would make is that it's not merely the people who are enrolled in the ACA exchanges today who are affected by high premiums. Of course, the 30 million people who are not enrolled in the exchanges because they're uninsured and find the premiums in those plans today unaffordable, those plans are even more unaffordable tomorrow for them than they were today.

POLLACKThree quick points about this, Susan. First, with respect to what these subsides are like and how significant they are, for a family of four that has $32,000 of income or less, the subsidies make sure that they don't spend more than 2 percent of their income on premiums. It goes up as your income goes up. It's what we call a sliding scale. The lower your income, the higher the subsidies and vice versa. For a family that has, say, $48,000 in income, they're going to be spending about 6 percent of their income on premiums.

POLLACKSo these still provide significant protection. Now, Julie made a very important point and that is one of the concerns that consumers have increasingly had with employer-sponsored coverage and all kinds of coverage is that out-of-pocket costs when you get care have been increasing, deductibles have been increasing. The Department of Health and Human Services has taken a step -- it's a modest step which I hope is going to be expanded to deal with that.

POLLACKAnd that is that they have created what they call a standardized plan that provides key services for people on a pre-deductible basis. So you can go see your primary care physician. You can get prescription drugs. Now, it is not required that these standardized plans be in communities across the country. I'm hopeful that will happen in the future, but it does mean that there is some potential for relief for people who are experiencing what Julie described a moment ago, who are paying high deductibles and don't feel very good about it.

POLLACKOne last thing I would say and that is the Affordable Care Act does provide protections for people so that they don't have to spend more than a substantial -- significant percentage of their income on out-of-pocket costs. Now, those only extend to people up to 250 percent of poverty, but they're still very significant.

PAGEBut Julie, there is a slice of America that gets caught, right? They're not low income enough to get a generous subsidy, but they don't make enough money to really devote thousands of dollars to healthcare insurance with their families.

ROVNERThat's true. I mean, anybody, you know, somebody who's at 401 percent of poverty, and believe me, I hear from lots of those people, I mean, for an individual, you know, it's just over $50,000 a year, which sounds like a lot of money, but then you're looking at unsubsidized premiums that can now be, you know, $700 a month or more if you're older, because, remember, older people pay more. So I had -- I saw a letter from, you know, a woman in her 60s, I mean, who just -- who simply can't afford her premiums, even though she's just over the subsidy level.

ROVNERI tried to find out exactly how many people that that were. It's not clear, but -- because there are people in the individual market who are not buying on the exchanges. It turns out some of those people could actually be getting subsidies. But it's probably a couple of million people.

PAGEPresumably because they're not aware they can get a subsidy if they went through the government website. We're going to take a short break. When we come back, we're going to talk about the debate on the presidential campaign trail, what Hillary Clinton and Donald Trump would do about the Affordable Care Act, what changes they might propose and what they might be able to get through Congress. And we'll take your calls and questions, 1-800-433-8850 is our toll-free number. Our lines are open. Give us a call. Stay with us.

PAGEWelcome back, I'm Susan Page of USA Today, sitting in for Diane Rehm. And we're joined now by phone from Vermont by Joel Ario, he's managing director of Manatt Health Solutions. He's the former insurance commissioner for the states of Oregon and Pennsylvania. And he was the first director of the Office of Health Insurance Exchanges at the United States Department of Health and Human Services. Joel, thanks so much for joining us.

MR. JOEL ARIOHappy to be here, Susan.

PAGENow you've really worked with states to try to deal with problems that have arisen with the Affordable Care Act. What states are having the most trouble? Is there some -- are there characteristics that they share?

ARIOEach state is really unique. I can talk about a couple, one that has found a good solution, one that is still struggling, but I did have to make one comment, Susan, on the last segment. I kind of found myself drowning a little bit in the numbers that were going back and forth in that segment. And I've got to say as a former insurance commissioner, the problem that most bedeviled me of all of the insurance problems we faced was the consumer who had some kind of illness or who is getting a little older and couldn't get any insurance in the individual market.

ARIOWe have solved that problem now. That's a very important thing. That's 20 million new people covered. We do have, because we've brought all those people in, we do have these questions about stabilizing premiums. T here's no question but that we're not out of the woods on that yet. But I do think we've got to go back and say the market today because you can now get insurance, even when you have a pre-existing condition, is just so much better, so much more stable than it was, and I know that because I lived that problem for 15 years in the states.

PAGEWell, there certainly are some provisions of the Affordable Care Act that I think Americans really like and will be hard to get rid of if a Republican administration came in and wanted to repeal the no-pre-existing conditions rule or the rule that lets your kids stay on your health insurance until they're 26. I can tell you I used that one when my kids got out of college.

ARIOMe, too.

PAGEYeah, so there are ways in which the Affordable Care Act has done things, but we see these premium increases for the fourth year enrollment that opens up and for the previous years. Is that a problem, do you think? Is this a big issue?

ARIOThis is the first year, frankly, as somebody said before, that they'd gone up higher than health inflation for all the previous years, not really correct for the Affordable Care Act part, for the marketplaces, the individual market. But this year it is a big problem. There are high rate increases. And so to go back to your question, sorry for that little commercial I had to add in the beginning, but to go back to your question, Alaska is a state I'm working with right now.

ARIOThey were looking at 40 percent, 42 percent rate increases in a market that was already the highest priced in the country, Alaska, big state, not many people, delivery system is spread out, pretty tough place to do medical care. And so they had the highest prices in the country. A 40 percent increase would have just crushed them, really. And so the insurance commissioner went to work with her legislature. They passed a re-insurance program. This is something that the federal government offered everybody for the first three years as a way to help the carriers spread the cost of the most expensive cases.

ARIOIt's -- that program is now gone, as of the fourth year, that's one of the reasons for these rate increases, but Alaska picked it up at the state level, the legislature passed a bill to put $55 million into a re-insurance fund based on some taxing of insurance companies, and that took those rate increases from the low 40s down into the single digits. I think they ended up at about eight percent.

ARIOSo that's good for consumers in Alaska. It's also frankly good for the federal government because when the premiums go down, as Ron explained in the last segment, the government's costs go down, too, because the government rather than the consumer is bearing most of the cost of those premium increases for people who are getting subsidies. So Alaska is now in the process, this is why I'm working with, is to go to the federal government and say since we're saving you a lot of money, we would like you to pass that money back through to us, and at this point the federal government is saying yeah, that's a good idea, we want to entertain that idea.

ARIOWe're still working out the details, but that is an example of a model that other states could do.

PAGEOkay, so Alaska, there's a success story. Tell us about a state that's really struggling, not doing so well.

ARIOMinnesota, Governor Dayton, a strong supporter of the ACA, has been pretty outspoken recently about the fact that 50 percent rate increase in his state are not acceptable. He's called on his legislature to do something about it. They're talking about some kind of short-term aid to people who just simply can't afford those kind of rate increases. And then he's also -- has a task force that I worked on with folks out there last year that he may re-empanel to come in and, after we get through this short-term crisis with the 50-percent rate increases, really look at the longer-term solutions, and one of them is a public option.

ARIOMinnesota has something called Minnesota Care, which is a program for low-income people. They would like to extend that program to a larger number of people and also allow people that don't need financial assistance to buy into that program at full cost. And so that would again take a 1332 innovation waiver with the federal government. You know, Secretary Clinton has called for a public option.

ARIOI think most people who look at this at the federal level say not a lot of chance that that's going to pass federally. But, you know, maybe we ought to let some states experiment with that to see if does work. Maybe let's let some states experiment in a different kind of way. And so Minnesota, not sure they'll come to this conclusion, but they may come to the conclusion that they would like authority from the federal government to try a form of public option out there in Minnesota, my old home state, always been a health care leader, just try that option in Minnesota, basing it on the program they already have that could now extent to beyond the low-income population.

PAGESo Joel, let me ask you a last question. When you -- we've had some states where the governors, the state legislatures, have been very enthusiastic about adopting provision of the Affordable Care Act and participating, we've had other governors and state legislatures who have been very resistant, have done the minimum, have had their citizens participate in the federal exchange rather than set up a state exchange.

PAGEIs -- do we now see a relationship between success and hard times, between states where the leadership of the state took different approaches?

ARIOAbsolutely. If you look at the states where there's only a single insurer or even two insurers, none of those are the state-based exchange states, where the state has really dug in, the insurance commissioner and other people, have dug in to working carefully with the insurers. I'm a little hesitant on this issue because I get in trouble with some of my former colleagues, but I like to say that what my father taught me is true, you reap what you sow.

ARIOSo the states where they've really put the effort in, California would be the number one example of this, they have a pretty successful marketplace. The states where they tried to resist and fought, you know, they're in more trouble. It's -- that's the way of life. If you put the work in, you'll get the results.

PAGEJoel give us a grade. What grade would you give Obamacare at this point, as the fourth year of enrollment starts to open?

ARIOOh, that's a tough question, Susan. I don't usually like answering them. But I'll say a B because it's clearly reached critical mass, it's clearly going to survive, it's definitely not excellent yet, it needs to improve, but it's way past, you know, past -- pas a success point, and so a B, B-plus, somewhere in there.

PAGEAll right, Joel Ario, thank you so much for joining us.

ARIOThank you, Susan, bye-bye.

PAGEJoel Ario is managing director of Manatt Health Solutions. He's a former insurance commissioner for the states of Oregon and Pennsylvania. Avik Roy, let me ask you, what grade would you give Obamacare at this point?

ROYWell certainly I think you could give the exchanges a C-minus. There are parts of the ACA that are working better than others. For example I think the Medicare Advantage cuts, there were a lot of people predicted that those cuts would not succeed and that people would be moving out of that program at an alarming rate. That hasn't turned out to be the case. Medicare Advantage is doing pretty well, people are signing up for those plans, and the performance of those plans is very good.

ROYBut on the exchanges specifically, which is really the topic we're focusing on today, it's more of a C-minus or a D-plus because these premiums are so high and unaffordable, not just for people who are on the exchanges but people who are off them. I think, you know, one thing that's very important that when I'm listening to my friends Joel and Ron on this panel is there's a lot of talk about protections, and I think economically we have to understand that every time Ron uses the word protections, what a consumer faces is higher premiums for the most part.

ROYYes, some people benefit from subsidies, but work we've done at the Manhattan Institute shows that people whose incomes are above 250 percent of the federal poverty level, the increase in the underlying premiums overcompensates or overreaches the subsidies they're receiving. So if your premium goes up by $200 a month, and the subsidy you get is $150 a month, your net premium is still higher, despite the taxpayer subsidies, and that's a big problem for people at the upper end of that 250 to 400 percent of 500 percent of the federal poverty level.

PAGESo Ron, before you explain that, we've got a B, B-plus from Joel, we've got a C, C-minus from Avik. Where would you grade Obamacare at this point?

POLLACKI'm going to give you two responses to this. First, there are key provisions of this statute that I'd give an A to. You referred to two of them. One is we no longer discriminate against people who've got pre-existing conditions. There are about 130 million people in the country who have some form of pre-existing condition. That -- I'd give an A or A-plus.

POLLACKYou mentioned allowing young adults under 26 years of age to stay on their parents' policy, very important, I'd give an A. A really key provision of the Affordable Care Act is no longer can insurers say to somebody, if they're really sick, or they get into an accident, at some point we're going to cut off your coverage because you -- there's a lifetime or annual cap. I'd give that an A. I would say that preventing women from being discriminated against in terms of premiums, I'd give that an A.

POLLACKNow with respect to what we're focusing on today, I'd give an incomplete, and the incomplete, every piece of significant legislation always needs some improvement later on. I -- my best example of that is the Social Security Act of 1935, one of the most significant pieces of social legislation in the history of our country. And yet many people don't know when the Social Security Act passed in 1935, it failed to protect over half the women in the workforce, it failed to protect over two-thirds of the people of color in the workforce. Those things needed to be changed.

POLLACKBut what the Social Security Act of 1935 did, it created a foundation, a platform upon which we could build, and that's what's going to happen with the Affordable Care Act. We are going to see improvements, and Susan, if I may jump to something you asked about or said we were going to focus on, the politics of this are going to have a significant impact.

POLLACKAnd if the polls are right, and Hillary Clinton is the president, we're going to see a watershed change because no longer is it going to be credible for opponents of the Affordable Care Act to talk about repealing the Affordable Care Act. And what that means is there may be opportunities, I don't want to say it too strongly, there may be opportunities for bipartisan, incremental improvements, which I think can fix some of the problems that we're talking about today.

PAGEJulie, let's finish going around the table. Give us your grade.

ROVNERWell, I don't -- I don't grade things, I'm a reporter, but I will certainly agree that some parts of the law are working better than other parts of the law. But I think it's important to think about, when you think about the health care system, that, you know, you move something in one place, and it affects something in another.

ROVNERTwo of the things that I think, you know, both of my colleagues here have suggested are sort of successes may be contributing to these premium increases. One of them is letting kids up to age 26 stay on their parents' plans. Otherwise they'd be in the individual market, they'd be the young and healthy people, they would be helping keep these premiums down.

ROVNERThe other thing is a dog that didn't bark. Everybody assumed that businesses that were going to -- particularly small businesses were going to drop insurance and send people to the exchanges, where most of them could get subsidies. Well, that really hasn't happened, perhaps because the exchanges got off to such a bumpy start. But that was the main reason why they haven't reached the numbers that the Congressional Budget Office estimated. Again, workers tend to be healthier. That has also contributed to making a smaller, sicker risk pool in these markets.

PAGEI'm Susan Page, and you're listening to the Diane Rehm Show. We're taking your calls, 800-433-8850. Let's take a call. We'll go to Dallas, Texas, and talk to Stan. Stan, hi, you're on the air.

STANHi, thank you. I just want to make a comment, and I think y'all have addressed it, but I think I hear so many talks where, you know, we talked about Obamacare in isolation and the rise in individual market health care premiums is as much or more in many of the states than Obamacare, and I think you have to make that comparison virtually every discussion.

STANBut my question is, I'm very concerned about low-income individuals who are working at $7.25 an hour, and they do get subsidies, and, you know, 83 percent or so of people get subsidies in the silver plans, and if we just eradicate Obamacare, what happens to these people? I mean, there needs to be some provision for them. We had mass medical bankruptcies before Obamacare came in. That decreased markedly, it's not gone away. So what's going to happen if Obamacare is, you know, repealed? What happens to working individuals?

PAGESo Stan, let me ask you, do you work in the health care field yourself?

STANYes, I do.

PAGEWhat do you do?

STANWell, I'm a physician, retired, and I worked at hospitals and with health plans.

PAGEAnd from your -- the job that you do, have you seen big changes with -- since the passage of the Affordable Care Act?

STANYes, very big and ones that have not been talked about. There's a provision within the ACA, Obamacare, that is stimulating hospital systems and physicians and other people, post-acute providers, to create integrated networks or these managed care -- or not managed care organizations but, you know, organizations where the providers are actually working together in more integrated delivery systems. We've had a lot of gaps in care in our current system.

STANThey're also looking at different ways of reimbursing. The fee-for-service does drive up health care costs. And so we're trying to look at how we can adequately pay providers and hospitals to provide excellent medical care, high-quality care at affordable price. And Obamacare started that work. It's still incomplete, as one of the prior speakers said, but I think that's valuable work. I'd hate to see Obamacare repealed and losing that pressure.

PAGEAll right, Stan, thank you so much for your call. Avik, let me give you a chance to respond.

ROYSure. So I think one thing that's important to note in this conversation is that many Republicans have advocated for a long time ending the problem of medical bankruptcies. There are different ways to do that than the way that the ACA did it. For example John McCain in 2008 proposed a plan in which every American would have a tax credit. The tax credit would be large enough to fund catastrophic health care insurance that would ensure that no American suffered from medical bankruptcies.

ROYThe plan that House Speaker Paul Ryan has proposed, that -- a part of his suite of proposals called A Better Way, similarly proposes a refundable tax credit that would effectively end the problem of medical bankruptcy. So I don't think there's really a debate about whether we should tackle the problem of medical bankruptcies in America. The real debate is about the regulatory architecture of the ACA and whether that architecture does too much or too little to quote-unquote protect consumers or allow them to buy affordable health care at an affordable price.

PAGEYou know, Republican -- the Republican position in Congress is to repeal Obamacare. We've had I don't know how many votes, and maybe, Julie maybe you know.

ROVNERSixty-some.

PAGESixty-some votes to repeal Obamacare, which obviously isn't going to go anywhere while the president could veto that. Do you think that would be a good idea, to repeal Obamacare and start over again?

ROYWell, I think that to repeal Obamacare and do nothing is not viable, and I think there's -- there are very few people in the House of Representatives who agree that repealing Obamacare and walking away is the solution. I think what Republicans really are passionate about is reforming the system along lines that give consumers more choice and more control over their own health care dollars.

PAGEThat's Avik Roy, he's the co-founder and president of the Foundation for Research on Equal Opportunity. And we're also joined in the studio by Ron Pollack, executive director of Families USA, and Julie Rovner, senior correspondent for Kaiser Health News. She's the author of "Health Care Policy and Politics A-Z." We're going to take a short break. Stay with us.

PAGEWelcome back. I'm Susan Page of USA Today sitting in for Diane Rehm. We're talking about the Affordable Care Act, the challenges it's facing now, what possible solutions there might be under a new administration. And with me in the studio, Ron Pollack from Families USA, Avik Roy who has been a policy advisor to Mitt Romney, Rick Perry and Marco Rubio in their presidential campaigns. And Julie Rovner from Kaiser Health News. You know, we've gotten some callers and some tweets from people who are worried about what's happening for them.

PAGEBecause they work for small businesses or they own small businesses. Here's an email from Susan. Insurance companies are raising premiums or cutting coverage for policies they offer small business. And blaming the ACA. So even people provided insurance by their employer are paying higher premiums or the small businesses paying an ever increasing amount to cover their employees. For example, my husband's business, which employs fewer than 50 people, is faced with a 43 percent increase in insurance costs to keep the same coverage next year. Needless to say, that is unsustainable. Julie, what's happening with small businesses?

ROVNERUm, nothing good. This is, if you're talking about parts of the law that have an incomplete, this would be probably the first part of the law that you would look at. The idea, one of the ideas behind the Affordable Care Act, one of the many ideas, was to not just stabilize and fix the individual insurance market, but to stabilize and fix the small business market, which is much, much larger than the individual market. Now one thing we haven't talked about, that we really should is underlying healthcare costs.

ROVNEROne of the reasons the premiums are going up for everybody and premiums are going up for everybody, is that underlying healthcare costs are starting to go up a little bit faster. Now, there's an ongoing debate about there has been a huge slowdown in the increase in healthcare costs over the last five years. Whether that was due to the recession, whether that was due to the law, whether it was due to some combination of the two, which I think a lot of people have sort of settled on. We've seen a significant slowdown in healthcare inflation, but the last year or two, we're starting to see it pick up again.

ROVNERIn large part, there's some of these hugely expensive specialty drugs, cancer drugs, hepatitis C drugs. So, we're seeing that, but small business in general has had this problem over a long time, that they've been, they've been experience rated. They've been -- it's been difficult. The Affordable Care Act was supposed to fix that. There's something called the shop exchanges. That program basically never got off the ground.

PAGESo what's happening with people who either own small businesses, want to help out their employees by offering insurance but are finding this unsustainable as Susan said in her email? Are they just throwing their employees into the insurance exchanges?

ROVNERWell, people thought that they would. But many of them haven't. A lot of employers, even small, now small employers, remember, are not required to cover their employees. That's only for larger employers under the Affordable Care Act. So they still, they did have the option whether or not to offer insurance. They still have that option. They can, as you suggest, if their employees don't make that much, they can send them to the exchanges, where the employees would then get a tax subsidy. But that largely hasn't happened.

ROVNERI think employers, you know, we've discovered employers want to provide health insurance to their workers. It's a key benefit. It helps them to, you know, get and keep good workers, so it's a continuing problem.

PAGEHere's a tweet from Chris. Chris asks, what's the argument against allowing insurance companies to compete across state lines? Why can't they sell plans nationally? Avik, is that a good idea?

ROYWell, there's a University of Minnesota economist named Steve Parente who's published work suggesting that if there was an opportunity to have a multi-state insurance plans, that you could reduce premiums by around 10 percent. So, it could help on some level, because there are certain economies of scale, ability to send people to providers across states. For example, if you live in a state that spans -- or a city that spans two different states, like New York City or St. Louis.

ROYThere might be opportunities there to look at providers in different -- and doctors and hospitals in different areas. So there are opportunities, but it's not a magic bullet. And I think the degree to which Donald Trump and others say, oh, if we just allowed people to buy insurance across state lines that this would magically solve all the problems in our healthcare system. That's not correct. And I think it's important on this issue of small businesses to say that the ACA does affect the cost of healthcare for small business in two ways in particular.

ROYOne, there are aspects of the ACA's regulations that drive up the cost of health coverage in, for small business. Such as the under 26 mandate that we talked about before. And other mandates of the type of insurance that small businesses must offer their workers. Another way in which the ACA affects small businesses is that the ACA has accelerated the trend of consolidation among hospitals, physician practices and other healthcare providers through accountable care organizations and other things that have happened over the last several years.

ROYThe end effect of more consolidation and more large hospital systems that are regional monopolies, that they have the leverage to charge higher prices and insurers don't have the leverage to fight back.

PAGEJulie, why isn't it a good idea to eliminate, to be able to sell insurance across state lines?

ROVNERI have a whole video on this, by the way.

PAGEIs that right?

ROVNER(unintelligible) But a couple things. First of all, multi-state plans are not the same as selling across state lines. And there are multi-state plans. There were supposed to be multi-state plans in every state. I think that's not quite happened yet under the Affordable Care Act. And also, there is a provision in the Affordable Care Act that allows states that span, you know, if you have a metropolitan area that spans states, they can do these interstate compacts. But what, you know, candidate Trump is talking about on the trail, and what has been a Republican idea going back many years is the idea of letting somebody in New York buy a policy from, you know, Montana if they want.

ROVNERAnd the concern about that is that people will end up, the healthy people will go to the states that have the least regulation, and the fewest requirements, and buy, you know, sort of the cheapest plans they can. That will make their state's risk pool only sick people, will sort of drive this whole race to the bottom.

PAGEYou know, talking about what might change to make things better, Hillary Clinton has endorsed the idea of having a public option as part of the Affordable Care Act. Ron, how would that work?

POLLACKWell, state option -- a public option would allow a -- some competition with private insurers and the theory is that this would help to reduce costs. But Hillary has a variety of different proposals that she's offering. And there's an enormous contrast between what she's proposing and what Donald Trump is proposing. The Rand Corporation actually did a study, you know, Rand Corporation is a non-partisan organization. And they found that if Donald Trump were elected, 20 million people would lose health insurance.

POLLACKIf Hillary Clinton is elected, nine million people would gain health insurance. Now, there are a number of reasons for that. What Donald Trump would do, as he said so clearly, he would totally repeal the Affordable Care Act. What he would replace, instead of these tax credit premium subsidies that we've been talking about, is he wants to create a tax deduction, which is totally different than a tax credit. And it actually, tax deductions are most helpful to people at higher tax brackets than it is for people in lower tax brackets.

POLLACKStan asked a question, the fellow from Dallas, what's going to happen to people who have modest incomes? Bottom line is, they're the ones who are going to be at greatest risk. Because they now get the best subsidies. Hillary would increase those subsidies. Hillary wants to make sure that these provisions that Julie talked about before, about re-insurance and risk corridors, that these are extended. That will help to get costs down. She wants to curb prescription drug costs. That could be very helpful. And so there are a variety of things that...

PAGEThese are all very popular things you're talking about. You know, more services, more subsidies. But I wonder is Hillary Clinton proposing anything -- do we have to do something tough if -- that people may not like so much? If we're going to make the Affordable Care Act sustainable, work better, not see these premium increases?

ROYThis, this is the box that Hillary Clinton is in is that she's, philosophically, a fan of a lot of the protections, quote, unquote again, that Ron and Joel mentioned. But those protections drive up premiums. If you try to cap deductibles, that drives up premiums. So the real solutions that Hillary is offering are to subsidize these higher premiums more, which a lot of tax payers wouldn't be fans of. Or to, the only other thing she could do, which she isn't proposing, is to stiffen the penalty for not signing up.

ROYThat would, of course, be politically toxic, and so she's not proposing that. So she's kind of stuck. If she doesn't want to unwind the regulations that are driving up premiums, premiums will continue to rise. And if you're not willing -- if you're not able to back that up with stiffer fines for not participating, or larger subsidies for the people who do enroll, there's not a lot you can do to improve the functioning of the exchanges. So I worry that the long term performance of the exchanges is continue -- is the gap between the expectations of 2010 and the reality of 2017, '18, '19, '20 is going to continue to widen.

PAGEBut she, but she said yesterday that she was -- that she felt there was a need to address these premium increases. She said that yesterday on the campaign trail. How would she do that Ron?

POLLACKWell, she, she will do it in a number of ways. She will extend the protections that insurers who are enrolling sicker and older people and providing them with protections. She does want to increase subsidies. I have to say, you know, we could, we could reduce premiums significantly. Just, let's end all regulation. Let's say to those people who have pre-existing conditions, sorry, you're going to go back to what happened prior to the Affordable Care Act and insurers are going to be allowed to, you know, to keep you out of the insurance system.

POLLACKOr they could charge you an arm and a leg compared to people. Or we could say we're no longer going to stop insurers for arbitrarily establishing lifetime or annual caps. Obviously, when you say to an insurer, you can't establish those caps, that is going to have some impact on premiums. But these are kinds of things that the American public wants because it makes sure that you have real insurance. And the people who need insurance the most, people who are sick, people who have asthma, diabetes, high blood pressure. They now can get this protection.

PAGEAvik.

ROYYeah, so, again, apologies to my friend Ron, but he's created several straw men at once, that there's this binary choice between the way the ACA is designed and some dystopia in which people are dying on the street. There are other ways to expand access to health coverage and care that involve different designs and different structures than what the ACA provided. My new think tank, the Foundation for Research on Equal Opportunity, we launched with a publication called "Transcending Obamacare."

ROYWhich is a 100 page proposal to reform the healthcare system in ways that would cover more people than the ACA, cost less than the ACA, and improve the quality of care that people receive.

PAGEAnd I think we've put a link on our website to -- so that people can read that 100 page study if they'd like to. So there are ways to address, to expand Obamacare, to try to change Obamacare, to revise it. Julie Rovner, what's realistic? What could actually get through Congress in a new administration?

ROVNERWell, I think it depends on the Republicans, right? Until, even assuming that the House remains Republican, the Senate will be evenly split, one way or the other. It looks like it's going to be pretty close. So there will be a two or three vote margin for whatever party has it. So you, you know, so you're going to have a lot of filibuster threat in the Senate, whichever party is in the minority. And, you know, up until now, the Republican position has been the only thing that we could agree on is that we want the Affordable Care Act to go away.

ROVNERWe can't really agree on what to replace it with. Everybody says repeal and replace, but when you get to replace it with what, there really hasn't been any -- any formal plan until Paul Ryan's plan which is still pretty much of an outline. So, it, at some point, the Republicans are going to have to say, this is hurting our constituents. We're going to have to come in and work on fixing it. That hasn't happened yet. Maybe it will happen with a new President, maybe it won't.

PAGEIf Hillary Clinton is elected, are there things she can unilaterally, through executive orders, to address some of these? Or does this need to, in fact, get through Congress?

ROVNERThe Obama Administration has done a lot of things through executive order. In fact, there, you were talking about increasing the penalties. They've actually made it more difficult for people to get exemptions from the penalties, to get, you know, what are called special enrollment periods where they can sign up outside the regular open enrollment. Because the insurers were complaining that people were gaming it. So, I think almost as much has been done by executive order as can be. It's getting to the point where it really will need legislation.

PAGEI'm Susan Page and you're listening to The Diane Rehm Show. We have some callers who have been really patient. Let's go to Jeff in Wilmington, North Carolina. Jeff, thanks for holding on.

JEFFYes, I have Obamacare. It's not great, but it's better than what I had before, which was absolutely nothing. I spent three days in the hospital the year before Obamacare and I'll finally make the last payment on that this December. Thank God. We should have national health insurance, like the rest of the civilized world, rather than put everything into the profit centers of insurance companies. And I voted blue from top to bottom for the first time in my life last week. And I will continue to do that until something is done about healthcare.

PAGEYou know, Jeff, you're from North Carolina. That's a pretty critical state. You've got an important Senate race there and you're important in the Presidential contest.

JEFFI have even been driving people to the polls.

PAGESo, let, but let me ask you, so you have insurance now through an exchange? Is that how you've gotten your insurance?

JEFFYes, I bought it online, through the exchange. My spouse would not be covered if it weren't for that my income was high enough and hers was low enough that we could get a subsidy together. But there's no way we could have bought insurance otherwise.

PAGEAnd how much difference has this made in your life, that you've had insurance for the last couple of years?

JEFFWell, I haven't needed it, again. But if I ever go to the hospital again, in three days, my hospital bill was 24,000 dollars.

PAGEYeah.

JEFFSo, it's very, very easy to go broke with a simple accident, like I had.

PAGEYeah. Jeff, thanks so much for your call.

POLLACKAnd people like Jeff, who experience real difficulties affording health insurance, I mean, we've seen such a significant improvement with 20 million people who didn't have health coverage before, now have health coverage. Now, I think we can do a whole lot more. I hope we will do more, but that's an extraordinary improvement.

PAGEAvik, what do you think Republicans, say if Hillary Clinton may win on November 8th. Let's say she does, but Republicans continue to hold the House, which seems likely. Do you think Republicans are going to be in a mood to get off the, we have to repeal Obamacare, we won't negotiate changes? Or do you think this is the kind of debate that we've seen in the last couple of years, we're going to see going forward for the foreseeable future?

ROYI've long agitated for Republicans to embrace the principal and the policy goal of universal coverage, but achieve it through a more market oriented mechanism. And that's what "Transcending Obamacare," the plan I mentioned earlier in the previous segment, is about. I think the challenge for Republicans in Congress under a President Hillary will be, are they more afraid of their base and being challenged in primaries? Or are they more oriented toward serving the constituents they have?

ROYI think if they're oriented toward serving the constituents that they have, then they should look at targeted fixes, knowing that Obamacare is not going to be repealed under the President, second President Clinton. What are the targeted fixes that they could achieve? And I've published some op-eds on how one could do that. There are certain regulations that are driving up the premiums disproportionately. You could reform those or revise those in ways that would help people. I'd love to see them work with the President to do that.

PAGEBut if that's the question, the answer, for the last couple of years has been Republicans are more concerned about a conservative primary challenge than they, than they are about your alternative. Is anything going to change that?

ROYWell, it remains to be seen. I think the real interesting debate, not just on healthcare, but on many issues, is how do Republicans reconcile themselves to what happened this year? Are they concerned sufficiently the Republican Party has become dysfunctional and isn't seem -- doesn't seem to be capable of being a governing party. This is very important.

POLLACKI think that so much is going to depend on the civil war within the Republican Party.

PAGEYes, that will be important.

POLLACKThat's going to determine a great deal. But I will say this much, Susan. Is that there are a lot of different interest groups that represent different political persuasions, different constituencies that feel this is something they need to come together on. And I think that's going to be very helpful as, if assuming Hillary is President, she is going to need these various groups that have different, very different interests coming together. And I think that is going to happen, and that's going to help in Congress.

PAGEJulie, we're almost out of time. Tell us, do you see this log jam of, of -- between Democrats and Republicans on the issue of the Affordable Care Act breaking any time soon? Do you think it might with a new administration, a new Congress?

ROVNERI think Ron's exactly right. It depends what the Republicans sort of decide when they, you know, sort of try to put themselves back together. But I think at some point, they're going to realize that their constituents want help and they want them to do something.

PAGEJulie Rovner, Ron Pollack, Avik Roy. Thank you so much for joining us this hour on the Diane Rehm Show.

POLLACKThank you.

ROVNERThank you.

ROYThank you.

PAGEI'm Susan Page of USA Today sitting in for Diane Rehm. Thanks for listening.

After 52 years at WAMU, Diane Rehm says goodbye.

Diane takes the mic one last time at WAMU. She talks to Susan Page of USA Today about Trump’s first hundred days – and what they say about the next hundred.

Maryland Congressman Jamie Raskin was first elected to the House in 2016, just as Donald Trump ascended to the presidency for the first time. Since then, few Democrats have worked as…

Can the courts act as a check on the Trump administration’s power? CNN chief Supreme Court analyst Joan Biskupic on how the clash over deportations is testing the judiciary.